2. Demand, Supply, and Elasticity¶

Demand and Supply 1¶

Demand¶

- Markets, the institutions that bring together buyers and sellers, are always responding to events, such as bad harvests and changing consumer tastes that affect the prices and quantities of particular goods.

- Variables that affect demand include price, consumer preferences, prices of related goods and services, income, demographic characteristics such as population size, and buyer expectations.

- A higher price tends to reduce the quantity people demand, and a lower price tends to increase it.

- The quantity demanded of a good or service is the quantity buyers are willing and able to buy at a particular price during a particular period, all other things unchanged.

- A demand schedule is a table that shows the quantities of a good or service demanded at different prices during a particular period, all other things unchanged.

- A demand curve is a graphical representation of a demand schedule; it shows the relationship between the price and quantity demanded of a good or service during a particular period, ceteris paribus.

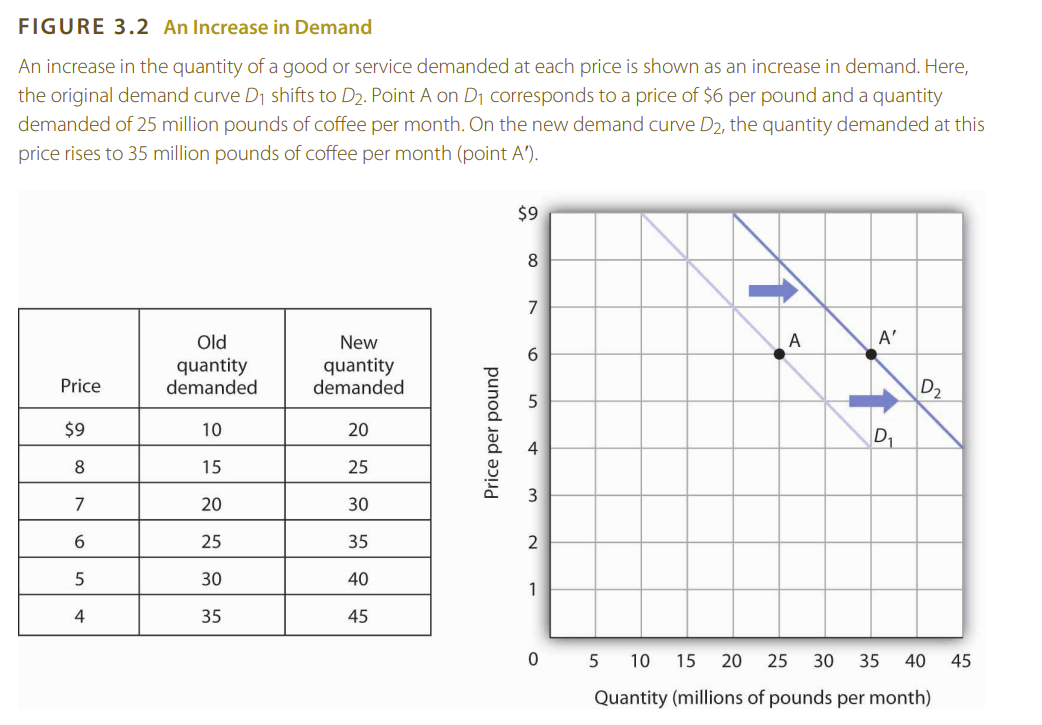

- A change in price, with no change in any of the other variables that affect demand, results in a movement along the demand curve (aka demand movement).

- The law of demand holds that, for virtually all goods and services, a higher price leads to a reduction in quantity demanded and a lower price leads to an increase in quantity demanded.

- If something else changes (other than price), there will be a shift in the demand curve (aka demand shift). To Right: Increase in demand; To Left: Decrease in demand.

- Example: People often eat doughnuts or bagels with their coffee, so a reduction in the price of doughnuts or bagels might induce people to drink more coffee. An alternative to coffee is tea, so a reduction in the price of tea might result in the consumption of more tea and less coffee.

- A demand shifter is a variable that can change the quantity of a good or service demanded at each price.

- The demand shifters are likely to include

- (1) consumer preferences: Customer push back against unhealthy products reduces the demand shifting the demand curve to the left.

- (2) the prices of related goods and services: Increase in the price of a substitute good will increase the demand for the good, shifting the demand curve to the right. Increase in the price of a complementary good will decrease the demand for the good, shifting the demand curve to the left.

- (3) income: Higher income increases the demand for normal goods, shifting the demand curve to the right. Lower income increases the demand for inferior goods, shifting the demand curve to the left; while decreasing the demand for normal goods, shifting their demand curve to the left.

- (4) demographic characteristics: E.g. more children means more demand for children’s clothing, toys, and food. An aging population may increase the demand for health care services.

- (5) buyer expectations: If buyers expect the price of a good to rise in the future, they may buy more of the good now, increasing the demand for the good and shifting the demand curve to the right.

- Complements:

- Complementary goods are goods used in conjunction with one another.

- Two goods for which an decrease in price of one increases the demand for the other. E.g. Coffee and doughnuts.

- Two goods for which an increase in price of one decreases the demand for the other. E.g. Coffee and tea.

- E.g. Tennis rackets and tennis balls, eggs and bacon, and stationery and postage stamps.

- Substitutes:

- Substitute goods are goods used instead of one another.

- Two goods for which an decrease in price of one decreases the demand for the other. E.g. Coffee and tea.

- Two goods for which an increase in price of one increases the demand for the other. E.g. Coffee and doughnuts.

- E.g. Cereals and eggs, CD players and Ipads, Pepsi and Coke.

- Normal Goods:

- A good for which demand increases as income rises and decreases as income falls.

- E.g. Cars, houses, and restaurant meals.

- Inferior Goods:

- A good for which demand decreases as income rises and increases as income falls.

- E.g. Bus rides, used clothing, and instant noodles.

- Alternatives that you only choose if you can’t afford the normal goods.

Supply¶

- Ceteris paribus, a higher price is likely to induce sellers to offer a greater quantity of a good or service.

- The greater the number of sellers of a particular good or service, the greater will be the quantity offered at any price per time period.

- Production cost is another determinant of supply. Variables that affect production cost include the prices of factors used to produce the good or service, returns from alternative activities, technology, the expectations of sellers, and natural events such as weather changes.

- Quantity supplied: The quantity sellers are willing to sell of a good or service at a particular price during a particular period, all other things unchanged.

- Generally speaking, however, when there are many sellers of a good, an increase in price results in a greater quantity supplied.

- Supply schedule: A table that shows quantities supplied at different prices during a particular period, all other things unchanged.

- A supply curve is a graphical representation of a supply schedule. Change in quantity supplied Movement along the supply curve caused by a change in price.

- Change in supply Shift in the supply curve caused by a change in a supply shifter.

- Supply shifters include:

- (1) prices of factors of production: An increase in production factors prices should decrease the quantity suppliers will offer at any price, shifting the supply curve to the left.

- (2) returns from alternative activities: If other activities become more profitable, more sellers will switch to those activities, reducing the quantity of the good or service offered at any price, shifting the supply curve to the left.

- (3) technology: technological advances that reduce production costs will increase the quantity of the good shifting the supply curve to the right.

- (4) seller expectations: If sellers expect the price of a good to rise in the future, they may withhold some of the good from the market, reducing the quantity offered at any price, shifting the supply curve to the left.

- (5) natural events: E.g. Storms, insect infestations, and drought. If a storm destroys a large portion of the orange crop, the supply curve for oranges will shift to the left.

- (6) the number of sellers: An increase in the number of sellers supplying a good or service shifts the supply curve to the right; a reduction in the number of sellers shifts the supply curve to the left.

Demand, Supply, and Equilibrium¶

- Model of demand and supply: Model that uses demand and supply curves to explain the determination of price and quantity in a market.

- Equilibrium price: The price at which quantity demanded equals quantity supplied.

- Equilibrium quantity: The quantity demanded and supplied at the equilibrium price.

- Surplus: The amount by which the quantity supplied exceeds the quantity demanded at the current price. No surplus exists at the equilibrium price or below.

- A surplus in the market for coffee will not last long. With unsold coffee on the market, sellers will begin to reduce their prices to clear out unsold coffee. As the price falls, the quantity demanded will increase, and the quantity supplied will decrease until it reaches the equilibrium point where quantity demanded equals quantity supplied and the surplus is eliminated.

- The prices of most goods and services adjust quickly, eliminating the surplus. Later on, we will discuss some markets in which adjustment of price to equilibrium may occur only very slowly or not at all.

- Shortage: The amount by which the quantity demanded exceeds the quantity supplied at the current price. No shortage exists at the equilibrium price or above.

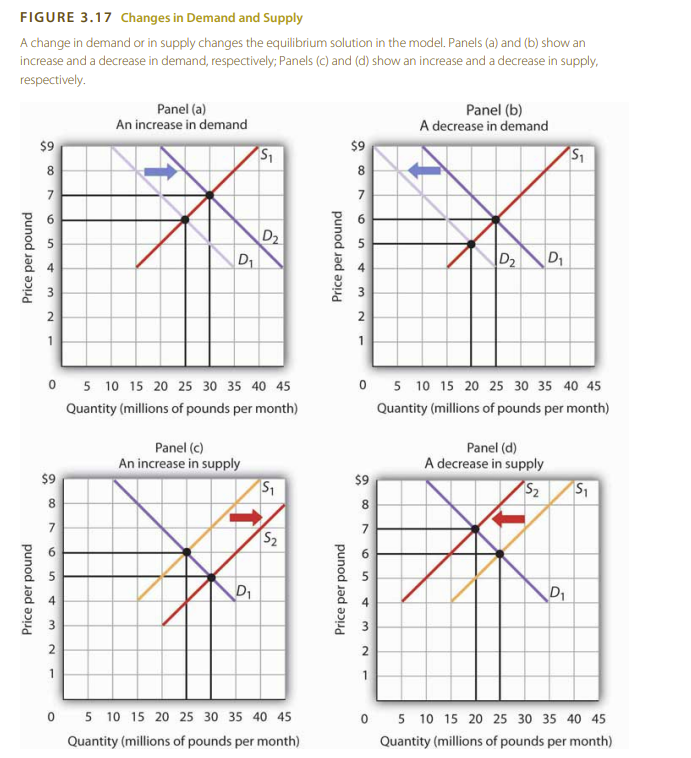

- A shift in a demand or supply curve changes the equilibrium price and equilibrium quantity for a good or service.

- Increase in demand: shifts the equilibrium price and quantity up.

- Decrease in demand: shifts the equilibrium price and quantity down.

- Increase in supply: shifts the equilibrium price down and the equilibrium quantity up.

- Decrease in supply: shifts the equilibrium price up and the equilibrium quantity down.

- Circular flow model: Model that provides a look at how markets work and how they are related to each other.

- A great deal of economic activity can be thought of as a process of exchange between households and firms.

- Firms supply goods and services to households.

- Households buy these goods and services from firms.

- Households supply factors of production (labor, capital, and natural resources) that firms require.

- The payments firms make in exchange for these factors represent the incomes households earn.

- Product markets: Markets in which firms supply goods and services demanded by households.

- Factor markets: Markets in which households supply factors of production (labor, capital, and natural resources) demanded by firms.

Introduction to Economics 2¶

Market Equilibrium 3¶

Elasticity: A Measure of Response 4¶

- Elasticity is the ratio of the percentage change in a dependent variable to a percentage change in an independent variable. If the dependent variable is y, and the independent variable is x, then the elasticity of y with respect to a change in x is given by: elasticity(x,y) = (% change in y) / (% change in x).

- A variable such as y is said to be more elastic (responsive) if the percentage change in y is large relative to the percentage change in x. It is less elastic if the reverse is true.

- Example: the dependent variable y is the number of passengers on a public transport system, and the independent variable x is the price of a ticket. If the price of a ticket rises by 10%, and the number of passengers falls by 20%, then the elasticity of the number of passengers with respect to the price of a ticket is -2.0.

- We know from the law of demand how the quantity demanded will respond to a price change: it will change in the opposite direction. But how much will it change? This is what elasticity measures.

- Elasticity (demand) = (% change in quantity demanded) / (% change in price). The price elasticity of demand is always negative.

- Sometimes you will see the absolute value of the price elasticity measure reported. In essence, the minus sign is ignored because it is expected that there will be a negative (inverse) relationship between quantity demanded and price.

- Arc Elasticity:

- The arc elasticity formula is used when you want to measure the elasticity of demand between two points on a demand curve.

- The formula is: eD = (∆Q/\(\bar{Q}\)) / (∆P/\(\bar{P}\) ).

- We should consider only small changes in independent variables. We cannot apply the concept of arc elasticity to large changes.

- It gives us the same answer whether we go from A to B or from B to A.

- Elasticity becomes smaller as we move downward the demand curve.

- The lower the price and the greater the quantity demanded, the lower the absolute value of the price elasticity of demand.

- Impact on total revenue:

- Total revenue is the price per unit times the number of units sold.

- The impact of a price change on total revenue depends on the initial price and, by implication, the original elasticity.

- It is not clear whether a change in price will cause total revenue to rise or fall.

- The price elasticity of demand may be useful in predicting the impact of a price change on total revenue.

- Based on the absolute value of the price elasticity of demand eD, we can classify goods into three categories:

- Elastic demand (>1):

- If |eD| greater than 1, then the demand is elastic.

- This means that the percentage change in quantity demanded is greater than the percentage change in price.

- Demand changes by a larger percentage than the price change (aka, demands changes a lot with price).

- Total revenue will change in the demand direction (opposite to the price direction):

- If price increases, total revenue will decrease.

- If price decreases, total revenue will increase.

- Unitary elastic demand (=1):

- If |eD| equal to 1, then the demand is unitary elastic or unit-price elastic.

- This means that the percentage change in quantity demanded is equal to the percentage change in price.

- Demand changes by the same percentage as the price change.

- Total revenue will remain the same.

- Inelastic demand (<1):

- If |eD| less than 1, then the demand is inelastic.

- This means that the percentage change in quantity demanded is less than the percentage change in price.

- Price changes by a larger percentage than the demand change (aka, demands changes little with price).

- Total revenue will change in the same direction as the price change (opposite to the demand change):

- If price increases, total revenue will increase.

- If price decreases, total revenue will decrease.

- Elastic demand (>1):

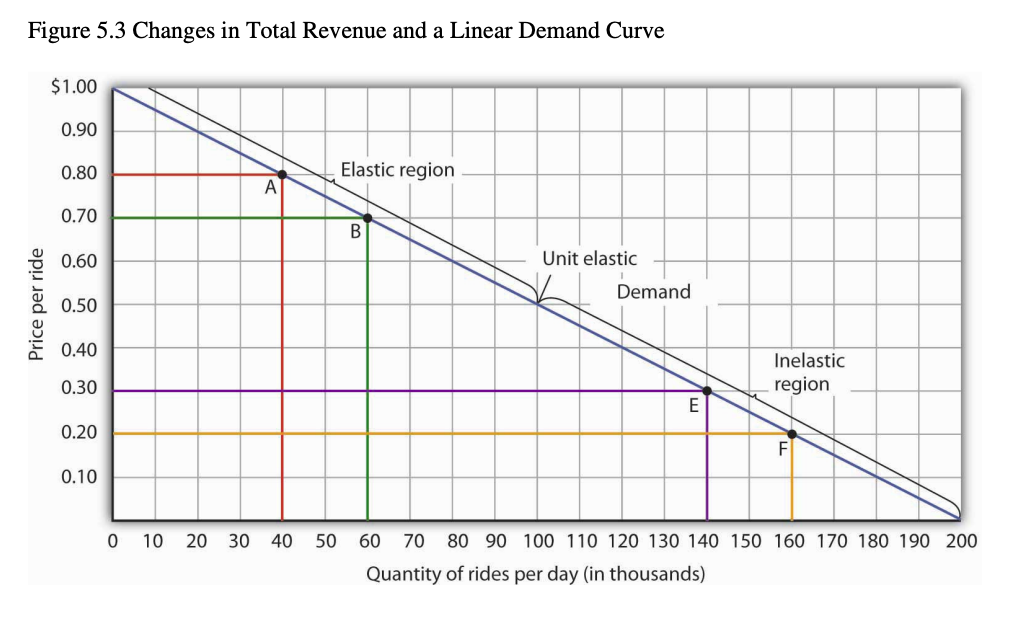

- A demand curve can also be used to show changes in total revenue.

- At point A, total revenue from public transit rides is given by the area of a rectangle drawn with point A in the upper right-hand corner and the origin in the lower left-hand corner.

- In general, demand is elastic in the upper half of any linear demand curve, so total revenue moves in the direction of the quantity change.

- At the midpoint of a linear demand curve, demand is unit price elastic.

- Determinants of the Price Elasticity of Demand:

- (1) the availability of substitutes:

- If there are lots of substitutes for a particular good or service, then it is easy for consumers to switch to those substitutes when there is a price increase for that good.

- The availability of close substitutes tends to make the demand for more price elastic. E.g. Ford cars (many substitutes).

- If a good has no close substitutes, its demand is likely to be somewhat less price elastic. E.g. gasoline (no close substitutes).

- (2) the importance of the item in household budgets:

- This effect is stronger when a good or service is important in a typical household’s budget.

- A change in the price of jeans, for example, is probably more important in your budget than a change in the price of pencils.

- More important items tend to have more price elastic demand.

- (3) time:

- More time allows consumers to adjust their behavior.

- More time after price changes, usually the demand becomes more price elastic.

- E.g. one day after electricity price increase, demand is inelastic as no one got time to respond. One year after, demand is elastic and many people have responded by switching providers or reducing consumption.

- (1) the availability of substitutes:

Income Elasticity of Demand¶

- eY = % change in quantity demanded / % change in income.

- We measure the income elasticity of demand, eY, as the percentage change in quantity demanded at a specific price divided by the percentage change in income that produced the demand change, all other things unchanged.

- A positive income elasticity of demand means that income and demand move in the same direction—an increase in income increases demand, and a reduction in income reduces demand.

- A good whose demand rises as income rises is called a normal good.

- If a good or service is inferior, then an increase in income reduces demand for the good. That implies a negative income elasticity of demand.

- Goods and services for which the income elasticity of demand is likely to be negative include used clothing, beans, and urban public transit.

Cross Price Elasticity of Demand¶

- The demand for a good or service is affected by the prices of related goods or services.

- eA,B = % change in quantity demanded of good A / % change in price of good B.

- It equals the percentage change in the quantity demanded of one good or service at a specific price divided by the percentage change in the price of a related good or service.

- A reduction in the price of salsa, for example, would increase the demand for chips, suggesting that salsa is a complement of chips.

- A reduction in the price of chips, however, would reduce the demand for peanuts, suggesting that chips are a substitute for peanuts.

- If two goods are substitutes, an increase in the price of one will lead to an increase in the demand for the other—the cross price elasticity of demand is positive.

- If two goods are complements, an increase in the price of one will lead to a reduction in the demand for the other—the cross price elasticity of demand is negative.

- If two goods are unrelated, a change in the price of one will not affect the demand for the other—the cross price elasticity of demand is zero.

Price Elasticity of Supply¶

Introduction to Economics 5¶

Price Elasticity of Demand 6¶

Price Elasticity of Supply 7¶

References¶

-

Rittenberg, L. & Tregarthen, T. (2009). Principles of Economics. Flat World Knowledge. Chapter3: Demand and Supply. https://my.uopeople.edu/pluginfile.php/1894528/mod_book/chapter/527762/PrinciplesOfEconomicsChapter03.pdf ↩

-

McAfee, R. P., Lewis, T. R., & Dale, D. D. (2014). Introduction to Economic Analysis. P.13-26. ↩

-

Khan Academy. (2012, January 2). Market equilibrium | Supply, demand, and market equilibrium | Microeconomics | Khan Academy [Video]. YouTube. https://youtu.be/PEMkfgrifDw ↩

-

Rittenberg, L. & Tregarthen, T. (2009). Principles of Economics. Flat World Knowledge.Chapter 5: Elasticity: A Measure of Response. https://my.uopeople.edu/pluginfile.php/1894532/mod_book/chapter/527770/Principles%20Of%20Economics%20Chapter%2005.pdf ↩

-

McAfee, R. P., Lewis, T. R., & Dale, D. D. (2014). Introduction to Economic Analysis. P.27-31. ↩

-

Khan Academy. (2018, November 15). Introduction to price elasticity of demand | APⓇ Microeconomics | Khan Academy [Video]. YouTube. https://youtu.be/FBWJYH8DZ1g ↩

-

Khan Academy. (2018, November 16). Introduction to price elasticity of supply | APⓇ Microeconomics | Khan Academy [Video]. YouTube. https://youtu.be/wi1x3sYHU6I ↩